It is clear that the rapid rise of the 10-year U.S. Treasury yield could have significant implications for active bond manager performance, as well as bond market volatility dynamics. But how might this affect the equity market? Another important role of U.S. Treasury yields is to act as a risk-free rate to compare to the market return, the excess return of which is known as the equity risk premium.

Coupled with rising yields and continuous record highs for the stock market, Exhibit 1 shows that the S&P 500® equity risk premium, measured here as the difference between the S&P 500 trailing 12-month earnings yield versus the 10-year U.S. Treasury yield, has plummeted over the past year, most recently entering negative territory. The last time the equity risk premium was below zero was following the burst of the Tech bubble during the early 2000s.

While the equity risk premium may indicate that equities seem relatively expensive compared to bonds, we do caveat that as of Jan. 21, 2025, Q4 2024 S&P 500 earnings season has started off on a solid note, particularly among the big banks, and if earnings growth continues, that might help to support current valuations.

We can also analyze equities and bonds from an income lens by comparing the market’s dividend yield to 10-year U.S. Treasury yields. Exhibit 2 illustrates that the yield on the 10-year U.S. Treasury of 4.6% has significantly outpaced the S&P 500 trailing 12-month dividend yield, which has declined over the past couple of decades to 1.3% as of Jan. 17, 2025.

Bonds may seem relatively better positioned from a valuation and income vantage point, but their diversification potential is also interesting to examine. We observe in Exhibit 3 that correlations between equities and bonds, as measured by The 500™ and S&P U.S. Treasury Bond Current 10-Year Index, have recently turned negative. After witnessing positive correlations for most of 2024, this reversal, if sustained, might be indicative of a tailwind for enhanced risk-adjusted performance for combinations of both asset classes.

As we enter a new presidential regime, filled with many uncertain variables, we may not know the future trajectory of bonds or equities, but understanding their historical value, income and diversification characteristics could aid investors to adapt accordingly.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

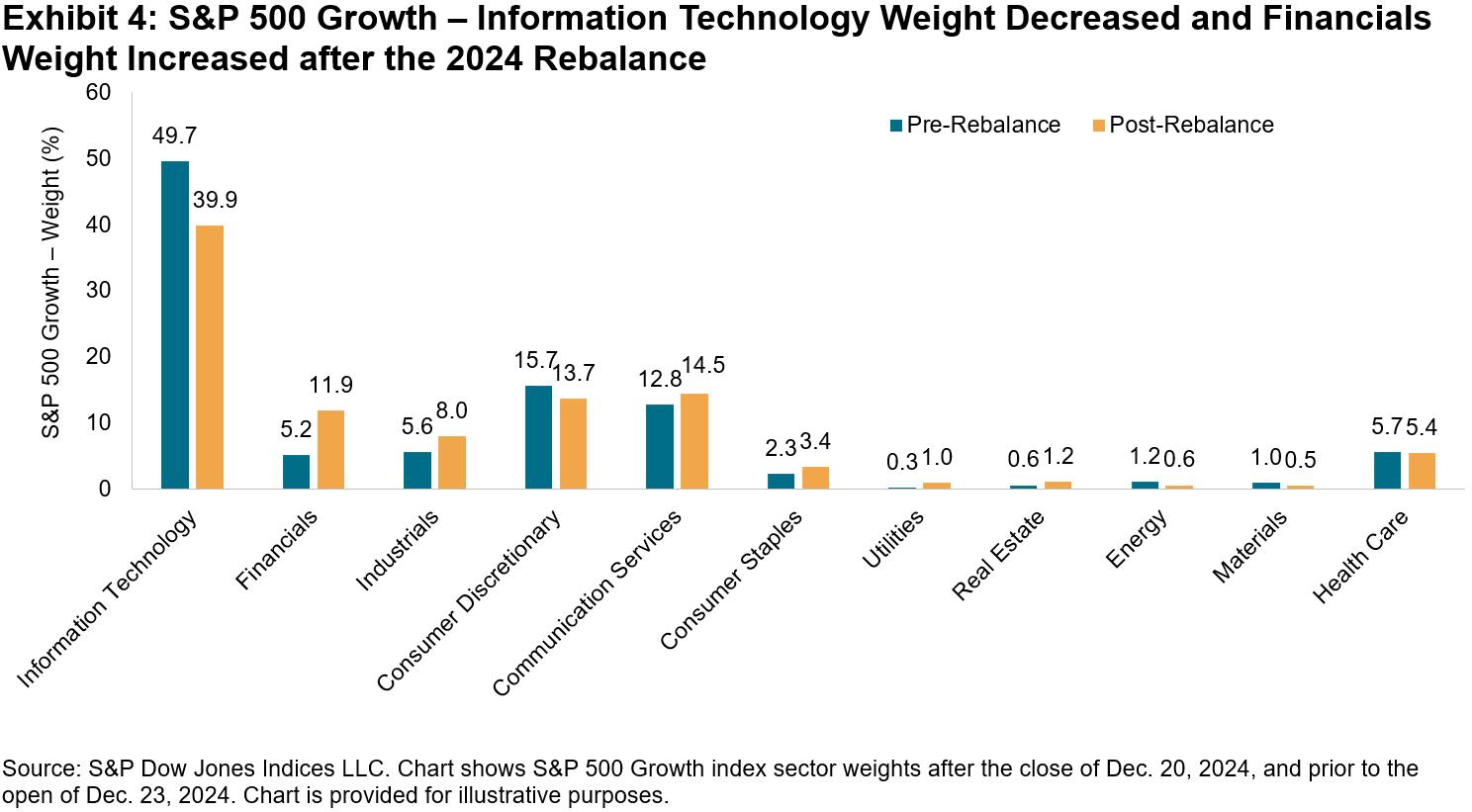

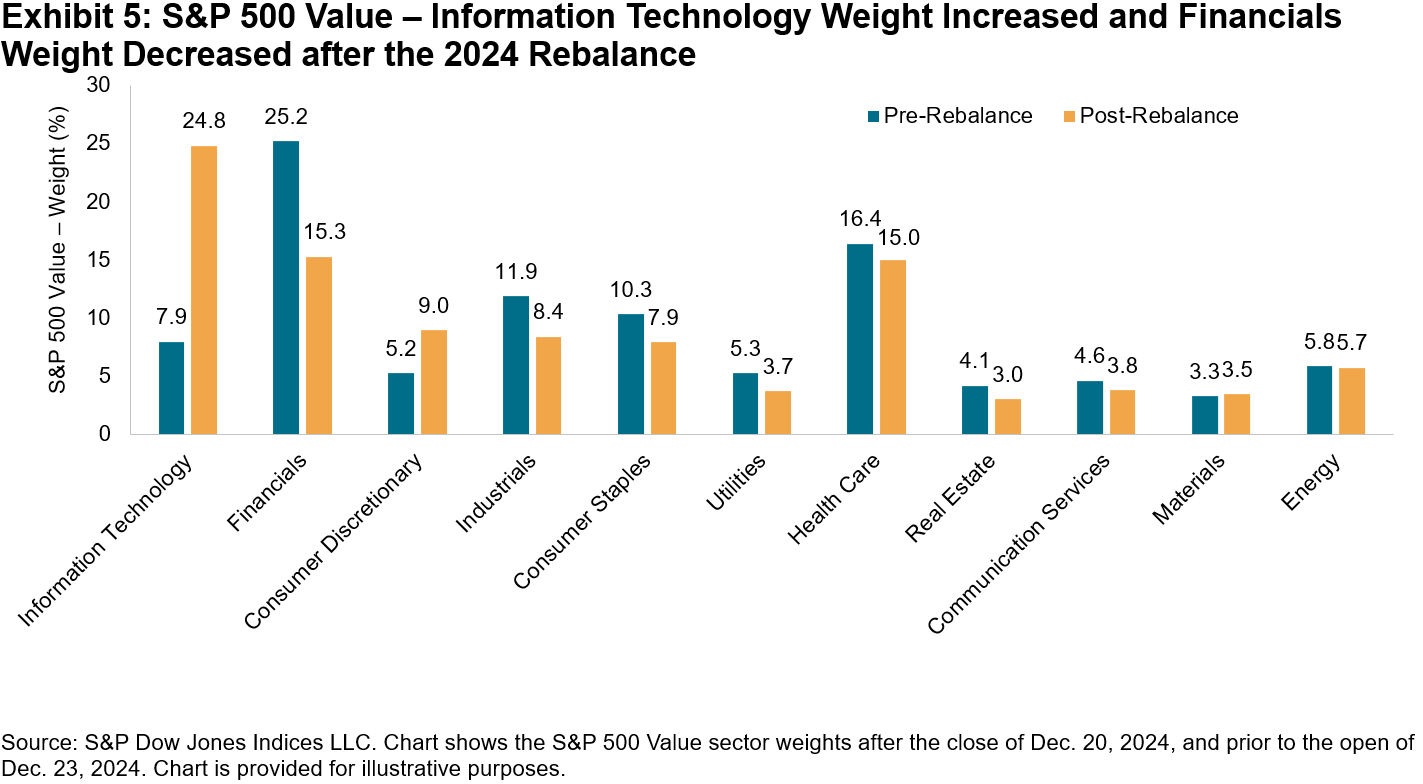

Notably, three of the five largest S&P 500 Growth companies pre-rebalancing—Apple, Microsoft and Amazon (representing 31.3% of the S&P 500 Growth’s weight)—moved to the blended basket. These companies migrated due to a decline in their Growth Score: Apple ranked lower in sales growth and earnings growth relative to the underlying index (the broader basket), while Amazon and Microsoft experienced declines in earnings growth and sales growth relative to the growth basket. Only Microsoft ranked lower in momentum relative to the broader basket.

Notably, three of the five largest S&P 500 Growth companies pre-rebalancing—Apple, Microsoft and Amazon (representing 31.3% of the S&P 500 Growth’s weight)—moved to the blended basket. These companies migrated due to a decline in their Growth Score: Apple ranked lower in sales growth and earnings growth relative to the underlying index (the broader basket), while Amazon and Microsoft experienced declines in earnings growth and sales growth relative to the growth basket. Only Microsoft ranked lower in momentum relative to the broader basket.